The recent announcement by President Donald Trump to impose tariffs on various countries has sent shockwaves through global markets, including our own. As an Australian investor, it’s natural to feel concerned about how these changes might affect your investments. Here’s a straightforward guide to help you manage this challenging period.

Understanding the Tariffs

President Trump recently escalated his tariff strategy, raising tariffs on Chinese goods to an unprecedented 125%, while temporarily reducing “reciprocal” tariffs to 10% for countries that have not retaliated against the United States. This marks a dramatic intensification of the US-China trade war, with China responding by imposing an 84% tariff on American goods, further straining global trade relations. Australia remains subject to a 10% tariff, which is the lowest level imposed by the Trump administration, reflecting its relatively small trade imbalance with the US.

Impact on Australian Markets

The Australian stock market, like many others, has experienced significant volatility following the tariff announcement. The ASX 200 index initially suffered substantial losses but managed to recover some ground by the end of the trading session. This volatility is a reminder that markets can be unpredictable, especially during times of global economic uncertainty.

Managing Your Investments

Keep Calm and Avoid Panic Selling

It’s essential to remember that market downturns are a normal part of investing. Panic selling during these periods can lock in losses and prevent you from benefiting when the market recovers. Historical data shows that investors who remain invested during downturns often fare better than those who try to time the market.

Diversify Your Portfolio

Diversification is key to managing risk. Ensure your investments are spread across different sectors and asset classes. This can help mitigate the impact of any single sector experiencing difficulties due to the tariffs.

Consider Defensive Strategies

In times of market uncertainty, defensive investments can provide stability. Consider allocating a portion of your portfolio to quality dividend-paying stocks or consumer staples, which tend to be less volatile during economic downturns.

Seek Professional Advice

If you’re unsure about how to manage your investments, consider consulting a financial adviser. They can provide personalised advice tailored to your financial goals and risk tolerance.

The Australian Dollar and Interest Rates

The Australian dollar has depreciated against the US dollar in recent times, reflecting broader market concerns about global economic stability. Meanwhile, the Reserve Bank of Australia has kept interest rates steady at 4.1%, awaiting clearer signs that inflation is returning to target levels. This decision reflects the central bank’s cautious approach to managing economic uncertainty.

Other countries have also voiced strong disapproval. China has vowed to implement “determined countermeasures” against the U.S., viewing the tariffs as an act of “unilateral intimidation”. The European Union, facing a 20% tariff, has pledged to adopt a collective stance and prepare counteractions if negotiations with the U.S. fail. EU Commission President Ursula von der Leyen warned that the tariffs would lead to increased uncertainty and serious repercussions for millions worldwide. Meanwhile, Canada and other nations are considering their own retaliatory measures to protect their economies. This global backlash underscores the potential for a broader trade conflict that could have far-reaching economic implications.

Conclusion

While the current market situation is challenging, it’s important to maintain a long-term perspective. By staying informed, diversifying your investments, and avoiding emotional decisions, you can manage these uncertain times effectively. Remember, market volatility is temporary, and history shows that markets have consistently recovered from downturns.

As an investor, staying calm and seeking professional advice when needed will help you make the most of your investments, even in the face of global economic challenges. Please feel free to contact us for tailored advice.

The 2025 Australian Federal Budget, announced by Treasurer Jim Chalmers on 25 March, outlines the government’s plans for the next financial year. While budget documents can be overwhelming, here’s a simplified look at the key changes that might impact your finances.

Income Tax Changes

The government has introduced new tax cuts to help ease the cost of living. From 1 July 2026, the tax rate for income between $18,201 and $45,000 will drop from 16% to 15%, and then to 14% in July 2027. For someone earning in this bracket, this means an extra $268 in your pocket by 2026 and up to $536 by 2027.

The table below summarises the proposed personal income tax rates and thresholds:

Taxable Income ($)

2024–25 & 2025–26 (%)

2026–27 (%)

2027–28 (%)

0 – 18,200

0

0

0

18,201 – 45,000

16

15

14

45,001 – 135,000

30

30

30

135,001 – 190,000

37

37

37

190,001+

45

45

45

While these cuts may seem small, they’re part of a broader effort to reduce taxes over time. Additionally, the Medicare levy low-income thresholds are going up by 4.7%, which could benefit lower-income earners.

However, Economist Peter Swan dismissed the tax cuts as a “complete joke,” arguing they won’t offset declining living standards.

Healthcare, Education, and Childcare

Healthcare is getting a boost with increased funding for bulk billing and cheaper medicines under the Pharmaceutical Benefits Scheme (PBS). Starting January 2026, PBS medicine costs will drop to $25 per prescription.

For students, there’s good news: a 20% reduction in outstanding student debts and an increase in the repayment threshold to $67,000 from July 2025. This means you’ll start repaying your loans later and owe less overall.

Childcare is becoming more accessible with the introduction of a “3 Day Guarantee” from January 2026. Most families will qualify for at least three subsidised days of childcare each week—no activity test required.

Energy Relief

The government has extended its energy bill relief program with an additional $1.8 billion commitment. This extension ensures that every household and around one million small businesses will receive rebates to help manage rising energy costs. Specifically, each eligible household and small business will get $150 in rebates, distributed as two payments of $75 each, over the second half of 2025.

Superannuation

The superannuation guarantee rate will increase to 12% from July 2025, helping Australians save more for retirement. Another change is “Payday Super,” which will require employers to pay super at the same time as wages starting July 2026. Super contributions will also apply to Paid Parental Leave for babies born after July 2025.

Also, the Budget reaffirmed its plan to implement a tax on superannuation balances over $3 million.

Housing Affordability

The “Help to Buy” scheme is expanding, allowing eligible buyers to access government equity contributions of up to 40%. A two-year ban on foreign investors buying established homes begins in April 2025, aimed at freeing up housing stock for locals.

Conclusion

The budget introduces measures like tax cuts, cheaper healthcare, student debt relief, childcare subsidies and energy relief designed to ease financial pressure on households. Initiatives around housing and superannuation aim for long-term benefits.

How much these changes affect you depends on your personal situation—whether it’s your income level, family needs, or housing plans. Please feel free to contact us if you would like to have a chat.

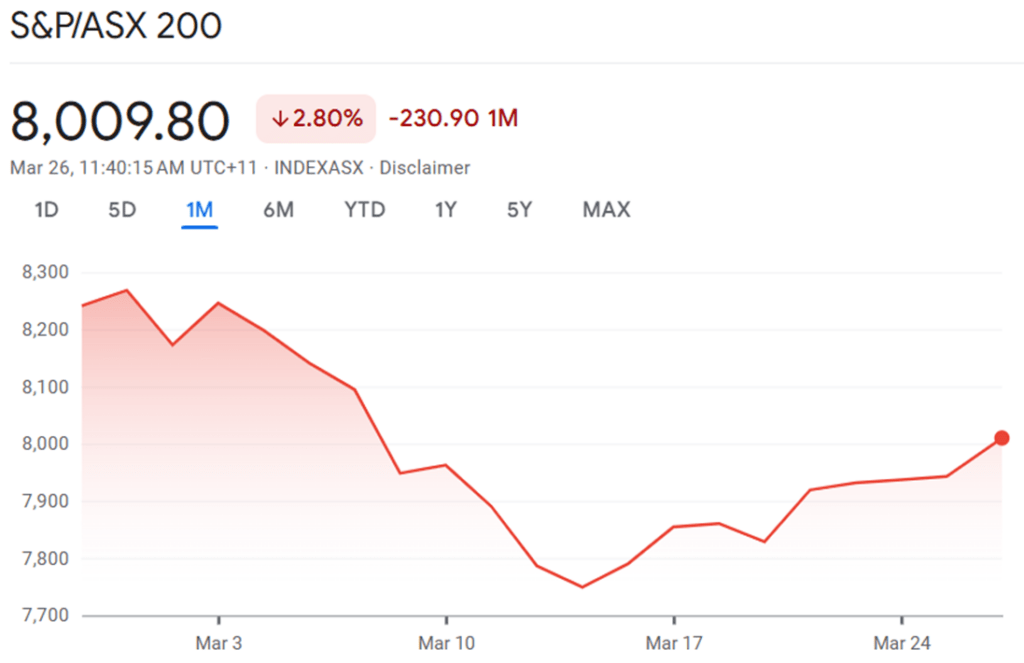

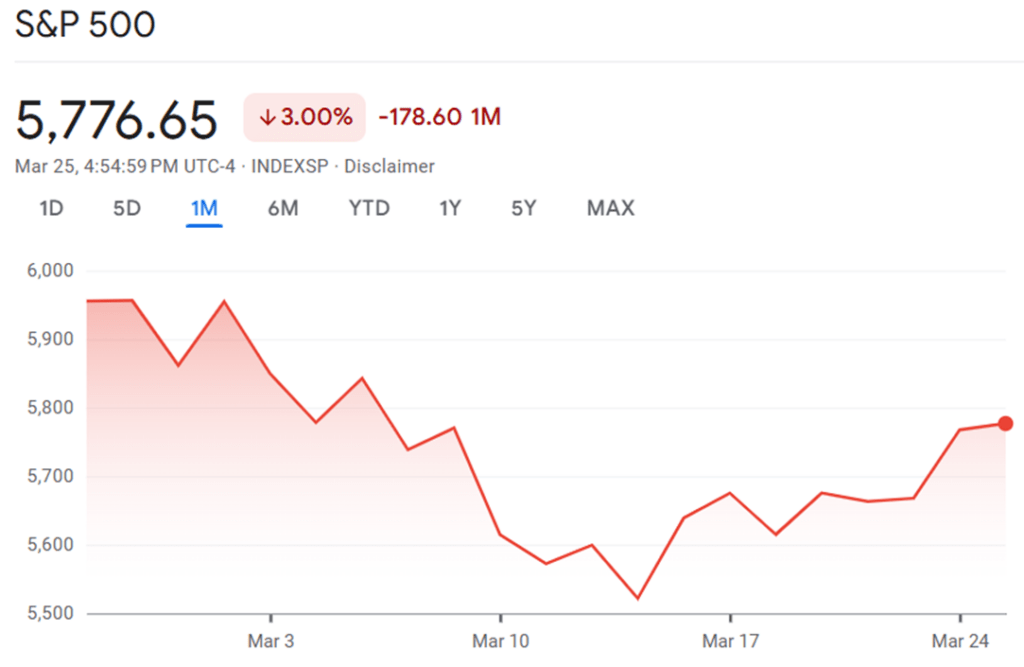

The month of March 2025 has proven to be a period of significant volatility for both the Australian and US equity markets. The S&P/ASX 200 is currently trading at 8,009.80 points, showing a monthly decline of 2.80% or 230.90 points, while the S&P 500 has experienced a similar downward trajectory with a 3.00% drop to 5,776.65 points. Both indices have followed remarkably similar patterns throughout March, characterised by sharp early-month declines followed by gradual recoveries toward month-end.

Source: Google Finance

The ASX 200 began March 2025 trading above the 8,250 level before embarking on a steady descent that intensified in the first half of the month. This downturn gained momentum as global markets reacted to intensifying trade tensions and shifting domestic economic indicators. By mid-March, the index had fallen to approximately 7,750 points, representing a significant correction from its early-month levels. This decline marked the fifth consecutive negative session for the index as of March 13.

The mid-month trough around March 13-15 found support in the 7,730-7,740 range, creating what analysts identified as a potential foundation for recovery. Indeed, the second half of March has witnessed a determined climb upward, with the index recovering nearly half of its earlier losses. By March 21, the ASX 200 was trading at 7,957 points and was poised to snap a miserable four-week losing streak. This recovery was partly fuelled by the absence of new tariff headlines and encouraging February labour force data that reinforced expectations of a potential Reserve Bank of Australia (RBA) interest rate cut in May.

A noteworthy contributor to the late-March recovery was the supermarket sector, following Australian Competition and Consumer Commission (ACCC) findings that concluded major retailers Woolworths and Coles should not be forcibly broken up. This news triggered substantial gains, with Woolworths surging 5.1% to $29.58 and Coles rallying 3.5% to $19.20 on March 21. The strength in these consumer staples provided important ballast to the broader market during an otherwise challenging period.

The release of the Australian Federal Budget on March 25, 2025, by Treasurer Jim Chalmers has added another dimension to market considerations. The budget included several significant funding allocations that could impact various sectors in the coming months. On Wednesday, March 26, the ASX 200 rose 0.7% or 53.7 points to 7,996.20 in early trading, briefly surpassing the 8,000 mark for the first time in two weeks. This upward movement was supported by a positive finish in New York and traders’ expectations that the budget would have minimal impact on potential interest rate cuts.

Whilst the full market reaction to the budget is still unfolding, initial responses suggest investors were largely prepared for the announcements. The modest upward movement in the ASX 200 in the final days of March indicates that the budget did not contain significant surprises that might have disrupted the recovery trajectory. However, the fiscal outlook will likely continue to influence sector-specific performance in the coming weeks as investors digest the full implications of the government’s spending priorities and economic forecasts.

Source: Google Finance

The S&P 500 has followed a remarkably similar pattern to the ASX 200 during March 2025. Beginning the month near 5,950 points, the index experienced a sharp decline that accelerated in early March. By March 13, the S&P 500 had officially entered correction territory, defined as a 10% drop from its most recent peak. This pronounced sell-off was primarily triggered by US President Donald Trump’s introduction of new tariffs on trading partners, which sparked fears of a potential global trade war.

Market anxiety intensified when President Trump acknowledged that there could be a “period of transition” after the tariffs were implemented, which many investors interpreted as a tacit admission that economic disruption was expected. This contributed to the steep mid-month decline that saw the index bottom out around 5,500 points, representing one of the sharpest corrections in recent years.

The second half of March has witnessed a notable recovery effort, with the S&P 500 climbing approximately 2.64% from its March 13 trough. This rebound gained momentum following the US Federal Reserve’s decision to leave interest rates unchanged, which helped calm market nerves and restore some confidence in the economic outlook. By March 25, the index had recovered to 5,776.65, though still showing a 3.00% decline for the month.

The volatility has prompted high-profile market analysts to reassess their outlook. Goldman Sachs, which had previously forecast the S&P 500 to reach 6,500 points by the end of 2025, has revised its expectations downward in response to the changed economic conditions. This adjustment reflects growing concerns about the potential impact of trade policies on US corporate earnings and economic growth more broadly.

Trade tensions have emerged as the dominant influence on both markets during March. The introduction of new US tariffs had immediate ripple effects across global markets, with Australian sectors particularly vulnerable to export disruptions showing pronounced weakness. The correlation between the two indices also reflects the significant presence of multinational corporations on both exchanges, whose earnings are directly affected by changes in global trade conditions.

Conclusion

March 2025 has been a month of considerable volatility for both the ASX 200 and S&P 500, characterised by sharp early declines followed by meaningful but incomplete recoveries. The 2.80% monthly decline in the ASX 200 and the 3.00% drop in the S&P 500 reflect investor concerns about global trade tensions, though the late-month rebounds suggest a degree of resilience in market sentiment.

The Australian Federal Budget announcement has added another factor for local investors to consider, though its initial impact appears relatively measured against the backdrop of broader global concerns. As March draws to a close, market attention will likely remain focused on trade policy developments, central bank statements, and key economic indicators that might provide clues about the direction of both economies.

For investors, the parallel movements of these major indices serve as a reminder of the globally connected nature of modern financial markets and the importance of maintaining a broad perspective when assessing market risks and opportunities. The coming months will reveal whether these March patterns represent a temporary correction or the beginning of a more significant market adjustment.

The Residential Property Market

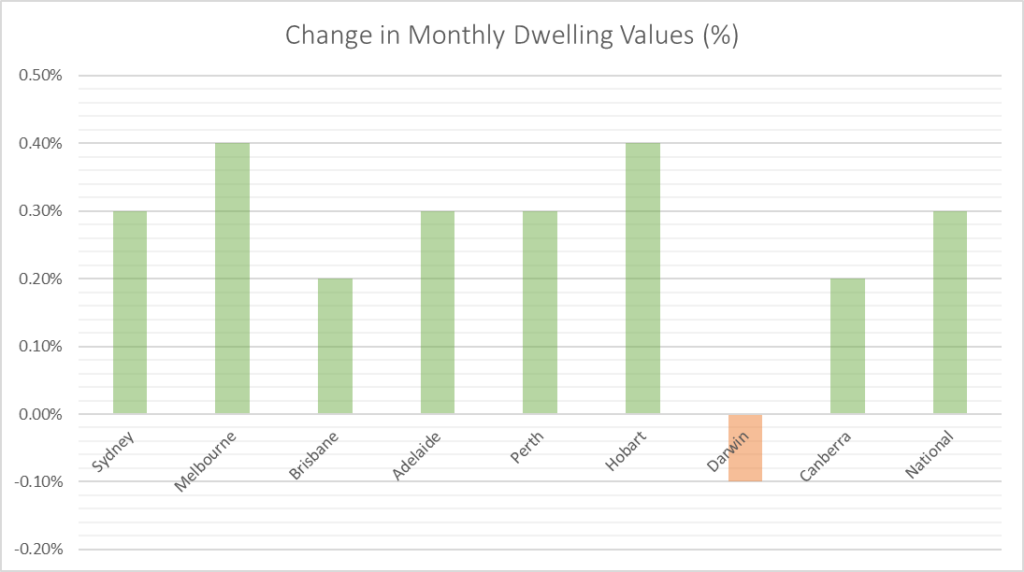

Australian housing markets have shown signs of recovery in February 2025, with values rising 0.3% nationally after a brief three-month downturn. This improvement appears to be driven by expectations of interest rate cuts and improved buyer sentiment rather than immediate changes in borrowing capacity. Melbourne and Hobart emerged as unexpected leaders in monthly growth, while previously strong performers like Brisbane, Perth and Adelaide experienced more modest gains. The rental market continues to moderate from previous highs, though still growing at twice the pre-pandemic average rate.

Housing Downturn Reverses with Broad-Based Recovery

The Australian residential property market has experienced a noteworthy shift in February 2025, with the CoreLogic national Home Value Index posting a 0.3% rise. This increase effectively breaks the short-lived downturn that lasted just three months and had pulled the national measure of home values 0.4% lower. The recovery was widespread, with nearly all capital cities and regional areas recording monthly gains, indicating a potential turning point in the market.

Melbourne and Hobart led the capital cities with both markets increasing by 0.4% in February. For Melbourne, this upturn is particularly significant as it breaks a streak of ten consecutive months of falling home values. This suggests that even markets that have been underperforming may now be finding their footing in the changing economic environment.

Interestingly, the previously strongest performing markets—Brisbane, Perth, and Adelaide—have recorded more modest gains between 0.2% and 0.3% for the month. This shift in momentum indicates a potential rebalancing across Australian property markets, with previously underperforming areas now showing stronger relative performance.

Premium Markets Leading the Recovery

A notable trend in February’s data is that the return to growth across Sydney and Melbourne is being driven primarily by the premium end of the market. Upper quartile house values are leading monthly gains in both cities after these high-value markets had previously recorded the sharpest declines. This aligns with previous research indicating that premium housing markets in Sydney and Melbourne typically respond most sensitively to interest rate adjustments.

CoreLogic’s research director, Tim Lawless, attributes the improved housing conditions more to improved sentiment than to any immediate enhancement in borrowing capacity. “Expectations of lower interest rates, which solidified in February, look to be flowing through to improved buyer sentiment,” he noted. This is further evidenced by improvements in auction clearance rates, which have risen back to around long-run average levels across the major auction markets.

Regional Markets Continue to Outperform Capital Cities

Regional housing markets maintained their stronger growth trend compared to capital cities in February. The combined regional index rose 0.4% over the month and 1.0% over the rolling quarter, compared to the 0.3% monthly rise and 0.4% quarterly decline seen in capital city values. This continues a pattern of stronger performance in regional areas that has been evident throughout much of the post-pandemic period.

However, there has been some variation in these trends, with Sydney, Melbourne, and Hobart now outpacing their regional counterparts in monthly growth. This suggests that the balance between capital city and regional markets may be shifting slightly as the recovery progresses.

Supply factors also appear to be supporting the improved market conditions. The flow of newly advertised listings across the combined capitals was tracking 4.7% lower than a year ago, and 1.5% below the previous five-year average. While total advertised supply levels are almost 1% higher than a year ago, they remain 7.9% below the previous five-year average. This reduced flow of fresh stock to market could be creating some upward pressure on prices, particularly if buyer activity is increasing with improved sentiment.

Rental Market Shows Seasonal Strength but Continued Moderation

The rental market has displayed a seasonal uptick with national rents rising by 0.6% in February, marking the strongest monthly gain since May 2024. However, this remains well below the 0.9% rise recorded in February 2024 and the 1.2% gain seen in February 2021 at the height of the rental boom.

On an annual basis, the slowdown in rental growth is more apparent. Nationally, rents rose by 4.1% over the 12 months to February, the slowest annual gain since March 2021, though still about double the pre-pandemic decade average of 2.0%. This moderation in rental growth is attributed to normalising net overseas migration and a trend towards larger household sizes, factors that have helped ease rental demand pressures.

The most significant slowdown in annual rental growth has occurred in Darwin, where house rents had previously boomed during the pandemic with a peak annual growth rate of 25.0%. The yearly change has now slowed dramatically to just 1.4% over the 12 months ending February. Similarly, substantial moderations in rental growth have been recorded across the unit sectors of Sydney, Melbourne and Brisbane, with annual growth rates dropping from peaks of 15-18% to around 3%.

Some cities have experienced a pickup in rental growth relative to a year ago, albeit from generally weak conditions. These include Hobart, Canberra, and the Darwin unit sector. Gross rental yields have lifted slightly over recent months, rising from a recent low of 3.65% nationally to 3.72%, reflecting that rents have been rising faster than house values since October 2024.

Market Outlook

While housing markets appear to have moved past the recent downturn, the recovery path seems likely to vary significantly across regions. The current rate-cutting cycle is very new and is expected to be drawn out rather than rapid. Financial markets are anticipating the cash rate to reach around 3.55% by the end of 2025, suggesting only two more twenty-five basis point cuts this year. Most economists project up to three more cuts, which would take the cash rate to 3.35%, still well above both the pre-pandemic decade average of 2.55% and the RBA’s estimated ‘neutral cash rate’.

Tim Lawless suggests that “Until home loan serviceability improves more substantially, it’s hard to see housing markets moving into a material growth trend”. However, markets that have experienced more significant downturns could be positioned for stronger recovery due to their renewed affordability advantage. Hobart (-11.9%), Canberra (-7.1%) and Melbourne (-6.4%) have recorded the most substantial declines from their recent peaks and may benefit from this relative affordability.

The supply-demand dynamic varies considerably across markets. Based on listing counts to February 23, inventory levels remain elevated in Sydney (+6.9%), Melbourne (+3.9%), Hobart (+25.2%) and Canberra (+6.8%) relative to the previous five-year averages. These regions, where prices remain below their recent peaks, may offer better opportunities for buyers. In contrast, Perth (-28.0%), Adelaide (-33.9%) and Brisbane (-21.5%) continue to face very low levels of homes available for sale, creating more competitive conditions for buyers.

A further lift in consumer sentiment would likely support increased purchasing activity, as historically there has been a close relationship between consumer sentiment measures and home sales volumes. While sentiment readings have risen substantially over the past six months, the trend has flattened in recent months. If sentiment returns to more optimistic levels, combined with the modest improvement in serviceability from rate cuts, buyer activity could strengthen further.

Looking forward, the pace and breadth of recovery will likely depend on the timing and extent of interest rate cuts, changes in consumer sentiment, and regional supply-demand dynamics. Markets that have experienced larger downturns may offer better value for buyers and potential for stronger recovery, while supply constraints in markets like Perth, Adelaide and Brisbane could continue to support price growth in these areas.

The property market’s response to these changing conditions will continue to unfold throughout 2025, with the current indicators suggesting a generally positive but measured outlook for Australian residential property.

Inflation and Interest Rates

Australia has seen significant shifts in inflation and interest rates, with the Reserve Bank of Australia (RBA) making its first rate cut since 2020. The cash rate now stands at 4.10%.

The Australian Bureau of Statistics (ABS) released its latest official inflation data for February 2025. The monthly Consumer Price Index (CPI) indicator showed an annual increase of 2.4% for the 12 months leading to February 2025. This figure indicates a continued moderation in the rate of price increases compared to higher levels experienced in previous periods, suggesting that the RBA efforts to curb inflation through interest rate adjustments are having a discernible effect. Excluding volatile items and holiday travel, the annual increase was 2.7%, with the annual trimmed mean also at 2.7%. Electricity prices saw a significant decrease of 13.2% in February 2025, likely due to government energy rebates. Consumer inflation expectations showed some divergence, with the Roy Morgan index at 4.9% for the week of March 17-23, 2025 , while Trading Economics reported a lower expectation of 3.6% in March 2025, the lowest since October 2021

As of March 2025, the official cash rate set by the RBA was 4.10% , following a 0.25% decrease on February 18, 2025. This reduction comes as a response to easing inflation, slower economic growth, and reduced wage pressures, signalling a stabilisation of the economy after a period of elevated interest rates. RBA Governor Bullock indicated that future rate cuts were not guaranteed. Market expectations, based on ASX futures, suggested an 8% probability of another rate cut in April 2025 . Major banks anticipated further rate cuts throughout 2025, potentially bringing the cash rate down to around 3.35% by year-end.

The Federal Budget for 2025-26, announced on March 25, 2025, projected a return to deficit, forecasting an underlying cash deficit of $27.6 billion for 2024-25, widening to $42.1 billion in 2025-26 . Gross government debt was projected to reach $1.22 trillion by 2028-29.

The Budget, amongst other items, includes a one-off 20% reduction in HELP debts, aiming to alleviate financial pressures on graduates and potentially increase disposable income. This measure, coupled with personal income tax cuts scheduled from July 2026, reflects the government’s strategy to stimulate consumer spending and support economic growth. However, these initiatives contribute to the projected budget deficit, highlighting the delicate balance between fiscal stimulus and maintaining sustainable public finances.

Additionally, the extension of the $75 quarterly energy rebate until the end of 2025 is expected to provide continued relief to households facing energy cost pressures. While this directly reduces certain components of the CPI, the broader impact of increased government spending on inflation remains a point of consideration. The RBA will need to monitor these developments closely, as the interplay between fiscal policy and monetary policy will be critical in steering the economy towards stable growth without reigniting inflationary pressures. The budget deficit and spending initiatives are expected to influence aggregate demand. While increased spending can lead to demand-pull inflation, measures like energy rebates directly lower CPI components. The increased deficit implies more government borrowing, potentially putting upward pressure on longer-term interest rates. Tax cuts and student debt relief could indirectly boost spending and potentially influence inflation.

Retirement is a significant chapter in life, offering the chance to enjoy the fruits of your hard work. But what does a comfortable retirement look like, and how can you prepare for it? For many people, it’s about finding the right balance between financial security, personal fulfilment, and peace of mind. Here’s how you can start shaping your ideal retirement.

What Does Retirement Mean to You?

Retirement is different for everyone. For some, it’s about travelling the world or buying a beachside home. For others, it’s spending more time with family, pursuing hobbies, or volunteering. The first step is to picture what your perfect retirement looks like. Ask yourself:

Do I want to downsize my home or stay where I am?

How often do I want to travel?

What hobbies or activities will I focus on?

Will I need to support family members financially?

By answering these questions, you’ll have a clearer idea of what you’re working towards.

Taking Stock of Where You Are

Once you know what you want, it’s time to assess your current situation. This includes:

Superannuation: Check your balance and whether it’s on track for your goals.

Savings and Investments: Consider any shares, property, or other assets you own.

Debts: Work out what you owe and how quickly you can pay it off before retiring.

This step helps you understand the gap between where you are now and where you need to be.

Building a Comfortable Retirement

A comfortable retirement isn’t just about money—it’s about having the freedom to live life on your terms. Here are some key areas to focus on:

Financial Security

The cornerstone of any retirement plan is ensuring you’ll have enough income to cover your needs and wants. This might come from superannuation, investments, rental income, or part-time work.

Health and Wellbeing

Staying healthy means enjoying more of what retirement has to offer. Think about private health insurance, regular check-ups, and setting aside funds for unexpected medical costs or aged care later in life.

Lifestyle Choices

Whether it’s learning a new skill, joining a club, or travelling interstate to see loved ones, having a plan for how you’ll spend your time is just as important as financial planning.

Making the Most of Australia’s Retirement System

Australia has a robust system designed to support retirees, but understanding how to use it effectively is key:

Superannuation: Make extra contributions if possible—it can make a big difference over time thanks to compound growth.

Age Pension: Learn whether you’re eligible and how much support you could receive.

Self-Managed Super Funds (SMSFs): If you prefer more control over your superannuation investments, this might be an option worth exploring with professional advice.

Creating an Income That Lasts

One of the biggest challenges in retirement is ensuring your money lasts as long as you do. A good plan balances regular income with long-term growth while accounting for rising living costs over time (inflation). You might consider:

Drawing down from superannuation gradually rather than in one lump sum.

Keeping some investments in growth assets like shares or property to outpace inflation.

Setting up an emergency fund for unexpected expenses so they don’t disrupt your plans.

Planning for Life’s Curveballs

No one likes to think about getting older or needing care, but planning ahead can save stress later on:

Research aged care options early so you know what’s available if needed.

Ensure your will and estate plans are up-to-date to make things easier for loved ones when the time comes.

How a Financial Adviser Can Help

Planning for retirement can feel overwhelming at times—but you don’t have to do it alone. A financial adviser can help by:

Clarifying your goals and creating a personalised plan to achieve them.

Helping you navigate complex systems like superannuation and pensions.

Offering strategies to protect your savings from inflation and market changes.

Giving peace of mind that someone is keeping an eye on your finances as life evolves.

Start Today — Your Future Self Will Thank You

The earlier you start planning for retirement, the easier it will be to achieve the lifestyle you want. Whether you’re just beginning to think about retirement or are only a few years away, now is the time to act.

Speak with our team of trusted financial advisers who understand your goals and can guide you through every step of the process.

Retirement isn’t just about stopping work—it’s about starting the life you’ve always dreamed of!

As Australia steps into 2025, there’s a careful sense of hope about the economy. Last year was tough, with slow growth and high prices, but things are looking up. Economic growth is forecast to improve, supported by easing interest rates, stabilising inflation, and rising household incomes. However, challenges such as cost-of-living pressures and labour market uncertainties remain in play. For investors, this presents unique opportunities in the property and dividend markets.

The Property Market: Riding the “Super Cycle”

Australia’s housing market is rebounding strongly in 2025, driven by structural supply-demand imbalances and rate cuts. Experts describe this as a “super cycle,” characterised by population growth, shifting demographics (e.g., smaller households), and construction delays. These factors are pushing property prices higher across most regions, except for Darwin and parts of regional Victoria.

Key Trends: Standalone houses are outperforming apartments, particularly in coastal areas, middle suburbs like Geelong and Wollongong, and regions such as Northern NSW and Southeast Queensland. Melbourne stands out as a value market after a 3.2% price drop last year, with outer suburbs like Craigieburn and Tarneit showing strong growth potential.

Risks: Oxford Economics warns that affordability could become a pressing issue as wages fail to keep pace with rising prices. Additionally, migration growth, which has supported housing demand post-COVID, is slowing but remains buffered by limited supply.

Takeaway: Investors should prioritise properties with scarcity value or those in undervalued markets like Melbourne. Regional hotspots such as Byron Bay and the Sunshine Coast also offer promising returns.

Dividend Investing: Beyond Chasing Yield

While term deposits and bonds now outyield the ASX 200’s average dividend yield of 3.5%, dividends remain a cornerstone of investment strategies when total returns are considered. In recent years, high-dividend indices have consistently outperformed broader market benchmarks due to their combination of income and capital gains.

Performance Trends: Mining companies like BHP have reduced payouts due to weaker commodity prices, but sectors such as retail (Wesfarmers, Coles) and travel (Qantas) have increased dividends.

Total Returns Matter: For example, a $10,000 investment in the ASX 200 in 2022 generated $383 in dividends by 2024 but achieved a total return of 13% when capital gains were included.

Takeaway: Focus on total returns by blending high-dividend stocks with growth sectors like technology or healthcare. Exchange-traded funds (ETFs) such as BetaShares’ High Yield ETF (ASX: ZYAU) provide diversified exposure to high-dividend companies.

Balancing Your Portfolio in 2025

Given the mixed economic signals this year, portfolio strategies should be tailored to individual risk appetites:

For Conservative Investors: Leverage low interest rates to invest in houses within growth corridors while targeting defensive dividend sectors like utilities or healthcare.

For Growth-Oriented Investors: Explore speculative property opportunities in rezoning areas like Melbourne’s outer suburbs or reinvest dividends into emerging sectors such as artificial intelligence or renewable energy.

Conclusion

Australia’s economic recovery in 2025 offers both opportunities and challenges for investors. The property market’s super cycle provides fertile ground for strategic investments in undervalued or high-growth areas. Meanwhile, dividend investing remains essential for building wealth but requires a focus on total returns rather than yield alone. Diversifying across asset classes will be key to managing risks while capitalising on this year’s unique investment landscape.

To ensure your investment strategy aligns with your unique financial goals and risk tolerance, it’s essential to seek personalised advice. Personalised investment management can significantly enhance your portfolio’s performance by tailoring it to your specific needs, preferences, and circumstances. Research by Vanguard shows that personalised investment advice can add up to 3% in net returns over time. If you’re looking to optimise your investments in property and dividends, consider reaching out to us for expert guidance. Our team can help you create a customised plan that not only maximises returns but also ensures your financial decisions are aligned with your long-term objectives.

The Reserve Bank of Australia (RBA) has made a significant move by cutting interest rates for the first time in over four years, reducing the cash rate from 4.35% to 4.10% in February 2025. This decision offers welcome relief to mortgage holders, and with the possibility of further rate cuts later this year, many are now considering how to make the most of this change. Here’s a straightforward guide to help you decide your next steps.

1. Understand Your Mortgage Type

If you’re on a variable-rate loan, your lender will likely pass on the rate cut sometime this month (if not the end of last month), reducing your monthly repayments. Contact your bank or check your banking app to confirm when the lower rate takes effect. For those with fixed-rate loans, however, your repayments won’t change unless you refinance. This could be worth exploring if lenders start offering sharper deals later in the year.

2. Explore Refinancing Opportunities

Banks often compete to attract borrowers after a rate cut. This means you might secure a lower rate or even cashback incentives by switching lenders. Keep in mind that refinancing costs, such as exit or application fees, can add up. Use comparison tools online to weigh your options, but don’t rush — waiting a few months could yield better terms if the RBA cuts rates again.

3. Stay Flexible

If you expect more cuts, avoid locking into long-term fixed rates right away. Variable loans let you benefit from future reductions, while splitting your loan (part fixed, part variable) balances stability and flexibility.

4. Use the Savings Wisely

A lower repayment frees up cash, but how you use it matters. Consider:

Paying down your mortgage faster: Keep paying what you did before the cut to reduce your loan’s principal.

Building savings: Park extra funds in an offset account or high-interest savings account.

Clearing high-interest debt: Prioritise credit cards or personal loans, which cost far more than mortgage interest.

5. First-Time Buyers: Proceed with Care

Cheaper borrowing costs might tempt you to enter the property market. While lower rates improve your loan capacity, remember that housing prices could rise if demand surges. Research local trends thoroughly and ensure you can afford repayments even if rates climb back up.

6. Plan for Uncertainty

Rate cuts are not guaranteed. Global economic shifts, stubborn inflation, or stronger wage growth could prompt the RBA to pause or reverse course. Deputy Governor Andrew Hauser has cautioned households to expect a cautious approach from the RBA, with any future rate cuts likely to be gradual and limited in scale. Unlike the aggressive reductions seen during the pandemic in 2020, the RBA is treading carefully to avoid reigniting inflation, which remains a key concern. Build a financial buffer to protect yourself against unexpected changes.

7. Look Beyond Your Mortgage

Lower rates can lift share and property markets. If you’re comfortable with risk, consider investing spare cash in diversified assets like ETFs or rental properties. Historically, REITs, and quality growth stocks often rally in falling-rate environments. Always align choices with your long-term goals.

Final Word

The RBA’s rate cut is a welcome shift for households, but its true value lies in how you use it. Whether you prioritise debt reduction, savings, or investments, thoughtful planning will help you stay ahead. It is always wise to budget conservatively and avoid overcommitting to debt, even as borrowing costs ease.

If you’re unsure about your options, please be sure to reach out to us. Professional guidance can tailor these strategies to your unique circumstances.

As we near the conclusion of our enlightening series, let’s delve into a pivotal aspect that consistently keeps you and your clients well-informed and thoroughly engaged: our Weekly Financial Articles. Crafted with precision by our dedicated team of financial content writers, these articles break down complex jargon into digestible, easy-to-understand language. Covering a wide array of essential topics—from the intricacies of the share and property markets to the nuances of insurances, superannuation/SMSF, retirement planning, estate planning, and pragmatic business advice—our content spans the entire spectrum of financial wisdom.

Why Our Financial Article Service is Indispensable:

Stay Ahead of the Curve: Our articles serve as your gateway to the latest trends, news, and strategies sweeping through the financial realm. They ensure you remain at the forefront of the industry, equipped with knowledge to navigate the ever-evolving financial landscape.

Foster Meaningful Conversations: Utilise our insights to ignite discussions, address your clients’ queries, and fortify the bonds of trust and reliability that underpin your client relationships. Our content is designed to spark curiosity and encourage informed dialogue.

Maximise Your Time: Recognising the premium on your time, we shoulder the burden of research and composition. This liberates you to dedicate your focus where it matters most—on your clients and their needs, ensuring they receive the utmost attention and care.

Embrace the Power of Financial Articles:

Seize this unparalleled opportunity to augment your expertise and concurrently offer immeasurable value to your clients, all without overextending yourself. Our weekly financial articles are more than just content; they are a resource, empowering you to broaden your horizons and enrich your advisory services. You can read a sample of these articles here: Demo Two website template

Join Our Mission to Demystify Financial Expertise:

This initiative is but one facet of our overarching commitment to support your journey toward delivering exceptional advisory services. Should you wish to leverage our meticulously curated content to its fullest potential, we invite you to reach out. Our aim is to furnish you with tools that not only enlighten but also embolden you and your clients on this financial voyage.

We eagerly anticipate seeing how you’ll harness these insights to cultivate growth and foster deeper engagement within your practice. Together, let’s navigate the path to financial literacy and success, making the complex world of finance accessible and understandable for all.

In Week 4 of our series, we spotlight a crucial tool for wealth management professionals: the Online Fact Finder. Understanding your clients’ financial circumstances, goals, and objectives is foundational to providing personalised advice. Our Fact Finder tool is designed to make this process as smooth and insightful as possible.

Benefits of Our Online Fact Finder:

Comprehensive Insights: With sections for personal details, assets and liabilities, superannuation, insurances, and more, you get a holistic view of your client’s financial health.

Efficiency and Accuracy: Streamline the data collection process, ensuring you have all the information you need in one place, accurately and efficiently.

Implementing the Fact Finder

Our tool is integrated into your premium website, ready for your clients to fill out at their convenience. This not only facilitates a deeper understanding of their needs but also enhances the client experience by making the process straightforward and accessible.

Our team will handle all of the setup with just a some important information from your firm including the Financial Services Guide, where the email notification should go to and your practice’s logo. Our fact finder or client questionnaire offers exciting features such as draft saving and reverse fact finder. Reverse fact finder is a feature where you can send a link to your client to update the information that you have already have in the system.

Next week, we’ll wrap up our series with an exciting offer that combines all the features we’ve discussed, designed to transform your online presence and client engagement.

Get Ready for a Deeper Client Connection

Our Online Fact Finder tool is just one piece of the puzzle in offering exceptional service. By utilizing it, you’re taking a significant step towards truly personalized wealth management.

If you’re intrigued by the potential of our Fact Finder and how it can benefit your practice, don’t hesitate to reach out.

Welcome to Week 3 of our exclusive series! We’re excited to share how you can streamline your appointment scheduling with Calendly integration, making it easier than ever for your clients to connect with you.

Introducing Calendly Integration

Our service seamlessly integrates with Calendly, linking directly to your MS Office or Google Calendar. This means your clients can view your real-time availability and book appointments without back-and-forth emails, enhancing their experience and saving you valuable time.

Easy Steps to Integrate Calendly:

Sign Up for Calendly: If you haven’t already, create a Calendly account and link it to your preferred calendar (MS Office or Google Calendar).

Set Your Availability: Customize your available times for meetings, ensuring clients can book sessions when you’re free.

Embed Calendly on Your Website: Calendly provides a simple code snippet that you can easily embed into your website, allowing clients to access your calendar and book appointments directly.

Why Choose Calendly?

Calendly offers a streamlined user experience, making it straightforward for clients to see your availability and schedule time with you.

It eliminates scheduling conflicts by automatically syncing with your calendar.

By reducing administrative tasks, you can focus more on what you do best—serving your clients.

We are not in any way affiliated with Calendly. We recommend it as an excellent tool for scheduling because we’ve found it to be incredibly useful in our own operations. It’s our hope that by sharing tools we trust and use, we can help enhance your practice as well.

Stay tuned for next week, when we’ll delve into our Online Fact Finder tool—a revolutionary way to understand your clients’ needs and objectives from the get-go.

Ready to Enhance Your Booking Process?

Implementing Calendly is just one of the many ways we’re committed to streamlining your operations and improving client satisfaction. If you have any questions or need assistance setting up, we’re here to help.

Looking forward to transforming your scheduling process together.

This week, we’re diving into a game-changer for your online client engagement: Live Chat Integration with TawkTo. Imagine offering your clients real-time assistance, answering their queries instantly, and making their online experience seamless. It’s not just about being there; it’s about being there when they need you the most.

Why Live Chat?

Immediate Response: Clients love quick answers. With live chat, you’re always just a message away.

Increased Engagement: Engaging clients in real-time leads to higher satisfaction and conversion rates.

24/7 Presence: Even when you’re off the clock, TawkTo’s AI capabilities ensure your clients are never left in the dark.

Simple Steps to Integrate TawkTo with Your Website:

Sign Up for TawkTo: It’s free! Just head to TawkTo’s website and create an account.

Customize Your Chat Widget: Tailor its appearance to match your brand and set up predefined responses to frequently asked questions for efficiency.

Install the Widget: Copy the unique code snippet provided by TawkTo and paste it into the HTML of your website. This small step will activate the live chat feature across your site.

Monitor and Engage: Use the TawkTo dashboard to monitor visitor activity in real-time and jump into conversations whenever needed.

Why Choose TawkTo for Your Website?

It’s free to use, making it perfect for businesses of all sizes.

Easy to install and customize, ensuring it blends seamlessly with your site.

Offers powerful features like chat history, visitor tracking, and more.

We are not affiliated with TawkTo in any way. We recommend TawkTo because we believe it’s a great tool and we use it ourselves. Our guidance is based on its ease of use and effectiveness in real-time engagement.

Next week, we’ll explore how to streamline your appointment scheduling with seamless calendar integration. Stay tuned!

Ready to enhance your client engagement with live chat? If you need assistance or have any questions, feel free to reach out. Let’s make your website as dynamic and responsive as the service you provide.